The Challenge

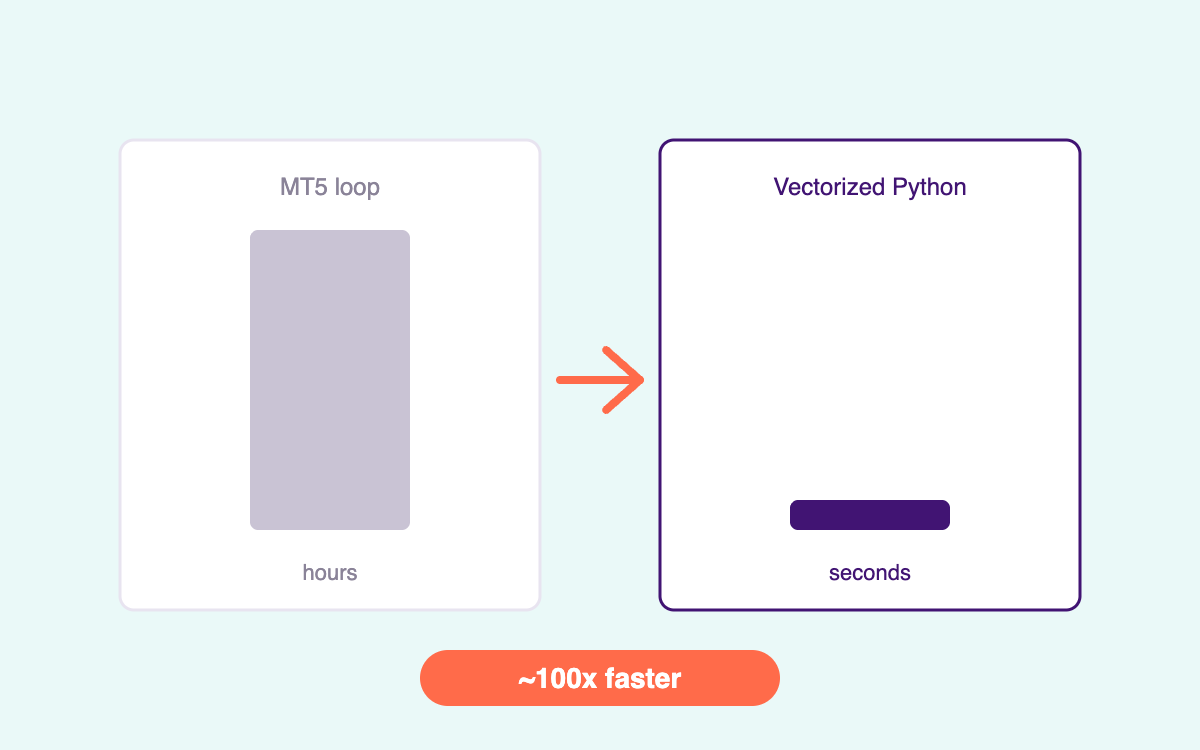

Strategy research dies when every backtest takes hours. Testing a parameter sweep in MT5’s built-in tester meant waiting overnight to learn one thing.

What We Built

- A vectorized backtesting framework in Python using array operations instead of bar-by-bar loops

- Parameter sweeps and optimisation runs across large historical datasets

- Results consistent with MT5 execution so findings transfer to live trading

Technology

Python · NumPy · pandas · vectorized computation

Outcome

Roughly 100x faster than the equivalent MT5 loop — turning overnight runs into coffee-break runs, so strategies get tested properly instead of assumed.

Want something similar built? Get a free consultation and fixed quote.